USDA loan refinance: Customizable Solutions for Reducing Your Loan Term.

USDA loan refinance: Customizable Solutions for Reducing Your Loan Term.

Blog Article

Maximize Your Financial Flexibility: Advantages of Funding Refinance Explained

Finance refinancing provides a critical possibility for individuals seeking to improve their financial flexibility. By securing a lower rate of interest rate or readjusting car loan terms, debtors can effectively reduce monthly settlements and boost cash circulation.

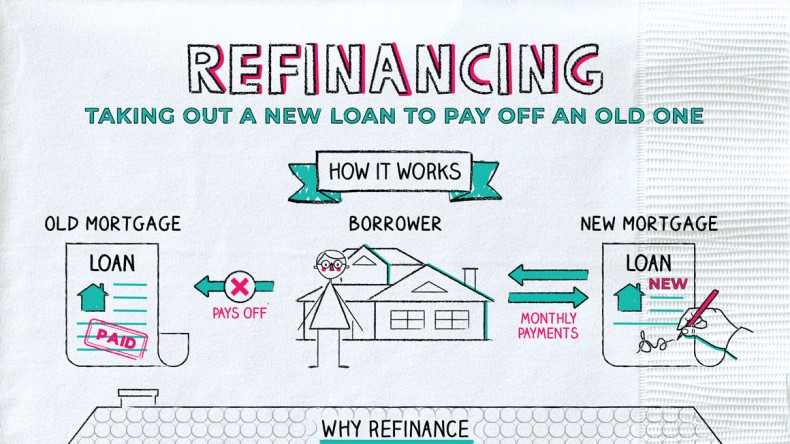

Comprehending Car Loan Refinancing

Comprehending loan refinancing is vital for house owners seeking to maximize their monetary circumstance. Financing refinancing includes changing an existing mortgage with a brand-new one, typically to accomplish far better finance terms or problems. This economic technique can be used for different reasons, including readjusting the financing's period, altering the kind of rate of interest rate, or consolidating financial debt.

The key goal of refinancing is often to reduce regular monthly settlements, thereby enhancing capital. Homeowners may also refinance to accessibility home equity, which can be used for considerable expenditures such as home restorations or education. In addition, refinancing can provide the possibility to switch over from a variable-rate mortgage (ARM) to a fixed-rate mortgage, giving even more security in monthly payments.

Nevertheless, it is important for property owners to evaluate their financial circumstances and the connected costs of refinancing, such as closing costs and charges. A comprehensive analysis can aid figure out whether refinancing is a sensible decision, stabilizing prospective savings against the preliminary expenses involved. Inevitably, recognizing funding refinancing encourages house owners to make enlightened choices, improving their financial health and leading the way for long-lasting security.

Lowering Your Rates Of Interest

Numerous house owners seek to lower their passion prices as a key motivation for re-financing their home loans. Reducing the rate of interest can dramatically decrease month-to-month settlements and total loaning costs, allowing people to assign funds towards various other financial goals. When rate of interest decline, re-financing provides a possibility to protect an extra beneficial loan term, inevitably enhancing financial stability.

Refinancing can lead to considerable cost savings over the life of the lending (USDA loan refinance). For instance, lowering a rate of interest price from 4% to 3% on a $300,000 home loan can result in countless dollars saved in passion settlements over 30 years. Furthermore, reduced rates may enable property owners to pay off their fundings more quickly, thus boosting equity and decreasing financial obligation faster

It is vital for property owners to analyze their current mortgage terms and market problems before making a decision to re-finance. Evaluating possible savings versus refinancing expenses, such as closing charges, is important for making an educated choice. By capitalizing on lower rate of interest, home owners can not just boost their monetary freedom however likewise produce a more secure economic future for themselves and their households.

Settling Debt Efficiently

Home owners often locate themselves handling numerous debts, such as credit report cards, individual fundings, and other monetary commitments, which can lead to increased anxiety and complex month-to-month repayments (USDA loan refinance). Combining financial obligation efficiently via loan refinancing supplies a structured visit this page solution to take care of these financial burdens

By re-financing existing financings right into a solitary, extra workable funding, house owners can streamline their settlement process. This method not only lowers the number of monthly repayments however can likewise lower the total rates of interest, depending on market conditions and specific credit report profiles. By consolidating financial obligation, house owners can designate their resources more effectively, maximizing money flow for crucial costs or cost savings.

Readjusting Funding Terms

Readjusting car loan terms can considerably affect a homeowner's monetary landscape, specifically after combining existing financial debts. When refinancing a mortgage, debtors can modify the size of the funding, rate of interest prices, and repayment routines, straightening them much more very closely with their existing monetary situation and goals.

For circumstances, extending the lending term can reduce regular monthly settlements, making it simpler to take care of cash circulation. This may result in paying even more passion over the life of the lending. On the other hand, opting for a shorter loan term can lead helpful hints to greater regular monthly settlements however significantly lower the total interest paid, allowing borrowers to develop equity more rapidly.

Additionally, changing the rates of interest can affect general affordability. Home owners might change from a variable-rate mortgage (ARM) to a fixed-rate mortgage for stability, securing lower prices, especially in a desirable market. Alternatively, re-financing to an ARM can supply reduced first repayments, which can be advantageous for those anticipating a boost in revenue or monetary conditions.

Improving Cash Money Circulation

Refinancing a home loan can be a tactical method to boosting cash money circulation, allowing borrowers to try here allot their funds better. By securing a lower rate of interest or prolonging the lending term, house owners can significantly lower their monthly home mortgage payments. This immediate decrease in expenditures can maximize funds for other essential demands, such as paying off high-interest financial debt, conserving for emergencies, or buying chances that can generate greater returns.

Additionally, refinancing can supply borrowers with the alternative to convert from an adjustable-rate mortgage (ARM) to a fixed-rate home loan. This change can stabilize month-to-month payments, making budgeting much easier and boosting financial predictability.

An additional avenue for enhancing cash circulation is through cash-out refinancing, where home owners can obtain against their equity to access liquid funds. These funds can be utilized for home renovations, which might enhance residential or commercial property value and, ultimately, capital when the home is sold.

Verdict

In final thought, loan refinancing offers a strategic opportunity to improve economic freedom. By decreasing rate of interest, consolidating debt, changing funding terms, and boosting capital, individuals can accomplish an extra favorable financial setting. This approach not just streamlines settlement procedures yet also advertises effective resource allotment, ultimately fostering long-term monetary safety and security and versatility. Embracing the advantages of refinancing can cause substantial improvements in overall economic health and security.

Report this page